With the doom and gloom of a recession not making the news these days, it’s important to reflect on what you did these past months. Your behaviour can often be the worst enemy of your portfolio.

If you went in cash, you missed a bounce, and now you will pay more to get back in. If you try to time the market, you will learn that it is very difficult and it’s not for everyone.

In the short run, the market is a voting machine but in the long run, it is a weighing machine.

Another point to be aware of is your risk profile and be very clear about the impact of the risk you are willing or not willing to take. The performance of your portfolio is based on the risk you will take, and your expectations need to be grounded on your risk, which defines the type of holding you will have.

When it comes to portfolio management, do not expect to just hold strong performers at all times. Your portfolio is like a hockey team. You start with your core, then you have your second and third line and then you manage the defense. Team managers are akin to portfolio managers which is what you are as a DIY investor. Trading your losers makes sense and building around your core is how you have a strong portfolio in all markets. Going back to the points above, depending on your skills and approach, you are either in the minors, the majors or the NHL. In my opinion, if you beat the index, you are playing in the NHL, but what matters is if you get what you need from your portfolio and not how it compares with the neighbour’s.

If you invest for income, look at it differently. Your portfolio should provide you with the income and keep up with inflation. If your portfolio is taking too much risk with high-income holdings and making you worried, it’s probably a team in the minor. What can I say? There is a simple math that defines how big your portfolio should be to generate a certain income with a certain yield. On top of that, one last component is the growth of the income, which must be higher than the inflation. Your rate of inflation, that is. You can start with the Canadian inflation rate, but at some point, your inflation rate needs to be understood when you retire.

Just like in hockey, there is a lot of data about the individual players and teams, which is the same for your stocks and your portfolio. Below are some recent data points I started using to ensure I do not cripple the growth of my portfolio with too many high-income investments and further down I share more of my analytics.

wpDataTable with provided ID not found!Stock Trades

I made one big decision this past month, and it was to drop 3M after two years. My decision came down to believing I could grow the value faster with another holding. We often focus on where we came from with a stock, but it is usually all about where you are going.

As it happens, JP Morgan Chase was discussed on a Jim Cramer Mad Money episode, and I decided to look further into it. At the current valuation, I felt it was a buy. I was a bit concerned with my exposure to banks but at the end of the day, if banks fail, so does a lot of the foundation of our economies. I am not one to hold gold bars in my basement.

Aside from the main swap mentioned above, I did the following transactions:

- I took a small profit from Apple and added to AbbVie. This is how I shift some of my growth profit towards higher-income stocks.

- I took a small profit from Microsoft and added to BlackRock.

A full position for my portfolio is when the stock reaches 5% of my portfolio weight. If it goes above 5.5%, I will consider taking profits.

Portfolio Management

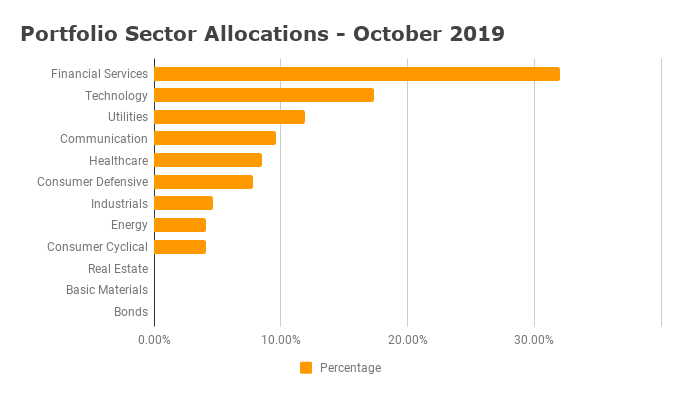

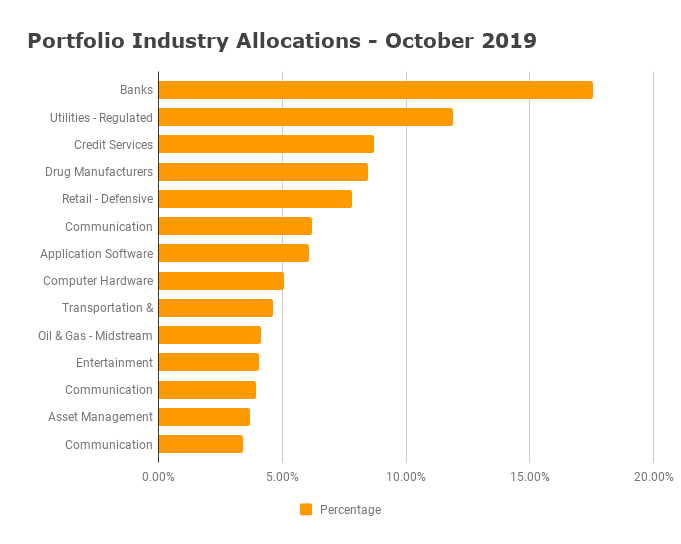

My portfolio analytics has evolved over the past decade. While I started with sector diversification, I now focus more on industry diversification. Focusing on the sector is easy because there are just around a dozen of them but there are far more industries and you won’t cover them all. My approach is to understand my sector diversification and then my industry diversification.

Over the past years, I have decided to not do rebalancing based on a sector ratio. Instead, I apply the concept of core holdings (first line) and secondary holdings (second and third lines). I also focus on the size of those holdings based on what I identify a core holding should represent. In looking at the graphs, I could show the separation between Canadian coverage vs US coverage. That would give you an idea of my portfolio composition by country.

Dividend Income

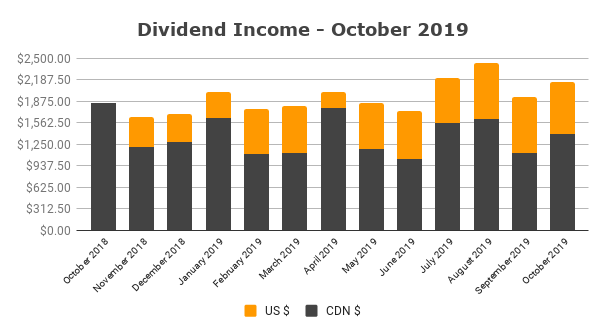

My October 2019 dividend income is $2,150. One shift not seen is that I have been withdrawing from the RESP account and that’s going to surface through a lower growth since the withdrawals will offset the growth. I always included RESP in the income since it’s part of the portfolio I need to manage but I am not going to be using it in retirement as you can see. As I start receiving less income from the RESP account, you will see that I earn quite a bit from my US holdings.

Note: I keep a 1 to 1 currency conversion with my US dividend income. It all goes back into US stocks.

The experience of managing the RESP account has been good as I looked at it as a mini-retirement account. The conclusion, if you are too focused on income stocks, it will cripple the growth of your portfolio. I realized that a while back and switched it ever so slightly towards banks and telecoms and it’s not that much different. The RESP account is my weakest account of all.

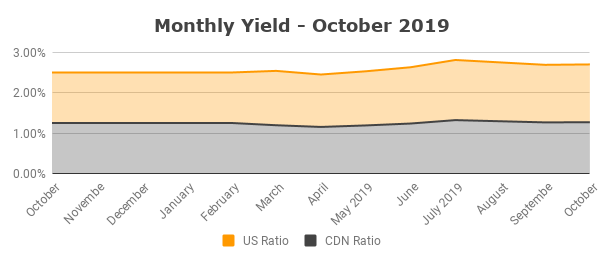

Below is the yield fluctuation based on the market value and the dividend payments. I am graphing it to see what it means to switch from dividend growth stocks to dividend income.